Using VesselsValue data, Dan Nash, Head of Ferry, RoRo and Vehicle Carrier, summarises the key trends of the Vehicle Carrier and RoRo markets in 2022. This article looks into the S&P and newbuild deals, factors driving trade and freight rates, and value changes across both sectors. You can read the full piece here.

Vehicle Carriers (PCTC, LCTC)

“2022 was a golden year for tonnage providers realising impressive stock gains from highly profitable charters, which went into overdrive after Lake Geneva (6,178 CEU, Jan 2015, Imabari) was extended to Nissan for 100,000 USD/Day in August on a twelve month deal. The same ship was fixed out at 40,000 USD/Day to Glovis at the end of 2021, equating to a +150% increase inside nine months…” Read more.

“Short supply fundamentals have another twelve months to play out possibly longer, until the sector is rebalanced by an armada of deliveries expected in 2024 and 2025, This will almost certainly bring down freight rates and asset values, unless China continues its amazing growth trajectory. The top of the cycle is near, but we are not quite there yet…”

RoRos

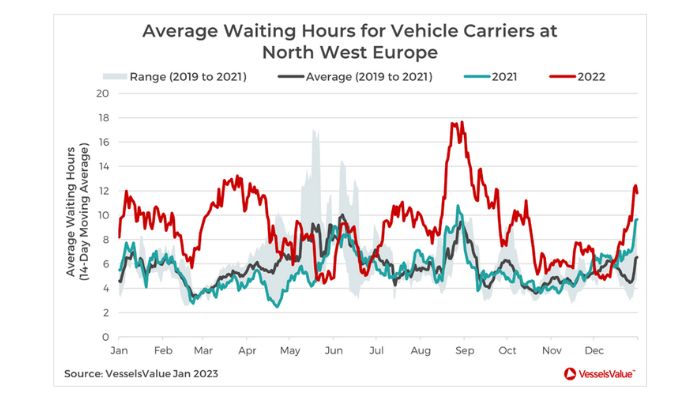

“Freight demand was particularly strong in the first half until Container demand collapsed from July, persuading newly gained shippers to return to LoLo (Lift on, Lift off) modalities. Nevertheless, sky high demand for car capacity in Europe kept OEMs interested in RoRos and Ferries for their regional ocean logistics, supporting asset demand…”

“In S&P, Midsize Gardenia Seaways (4,076 LM, July 2017, FSG) was sold BBHP (Bareboat Hire Purchase) by DFDS to Ulusoy in June for EUR 48 mil. Although not a straight sale, a good reference point for cousins in the sector. For Smalls, scrubber fitted Color Carrier (1,775 LM, January 1998, Damen Galati) was sold by Color Line to CLdN for EUR 12.5 mil in November…”

Press Release